Reason to trust

How Our News is Made

Strict editorial policy that focuses on accuracy, relevance, and impartiality

Ad discliamer

Morbi pretium leo et nisl aliquam mollis. Quisque arcu lorem, ultricies quis pellentesque nec, ullamcorper eu odio.

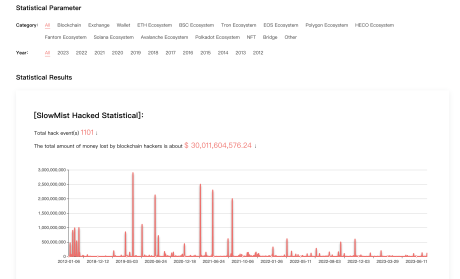

Due to the anonymity cryptocurrencies provide, the crypto industry is known to be targeted by hackers and other malicious players. This has left many wondering just how much digital currency has been pilfered from right under the nose of the industry over the years.

Now, the latest report by blockchain security firm SlowMist seems to have the answer. According to the recently released report, hackers and scammers have made off with a staggering $30 billion in cryptocurrency since 2012.

Details Of The Report

The SlowMist team analyzed 1,101 hacking incidents to determine how much crypto has been stolen to date and how they were stolen. Their findings show that hackers and scammers employ a variety of methods, with the top ones being contract vulnerability attacks, rug pulls, flash loan attacks, scams, leaking of private keys, and good old phishing attacks to gain access to people’s crypto accounts and wallets.

The most lucrative year for malicious players came in 2021 during the extended crypto hype, with over $9.7 billion stolen in 236 attacks.

In total, the amount stolen in the last decade came up to a little over $30 billion. And given that the overall market cap of all cryptocurrencies is now at $1.14 trillion, the amount reported stolen is over 2.5% of the total market cap.

Over $30 billion stolen in 10 years | Source: SlowMist

Exchanges And Ethereum Ecosystem Hit The Most

Exchanges have always long been a prime target for hackers looking to steal crypto due to their large holdings and the SlowMist report reflects that.

In total, over 118 attacks were carried out on exchanges, resulting in over $10.9 billion being lost. The biggest of these could be traced back to the $534 million lost in the 2018 Japanese exchange Coincheck hack and the 2014 Mt. Gov hack resulting in a loss of over $473 million.

Total market cap chart sitting at $1.139 trillion | Source: Crypto Total Market Cap on TradingView.com

In terms of attacks on blockchain ecosystems, Ethereum came out on top with 217 attacks and over $3.1 billion being pilfered away. This should come as no surprise, considering Ethereum is home to most Web3 projects.

The BSC and EOS ecosystems followed closely with 162 and 119 attacks, respectively. Additionally, over $200 million were lost in NFT attacks, while bridge attacks led to $2 billion in losses.

What’s Next For The Crypto Industry?

The staggering numbers in SlowMist’s report are a reminder that crypto, for all its promise, also has a dark side. However, attacks seem to have been slowing down as many projects have started to improve their security. With more than a trillion dollars at stake, reducing theft should be a collaborative effort across the entire crypto landscape.

According to the latest report by Beosin, a blockchain security firm, losses from Web3 scams and hacks dropped dramatically in H1 2023. Data from SlowMist’s report also shows that the total amount of money lost to blockchain hackers has been declining since 2021.